Take a mortgage as an example. If you close in the middle of the month, you might have a month or two before your first payment is due. When you make your first payment, you are paying in advance for the following period. Since no interest is collected between your closing date and your first payment due date, this interest is typically rolled into your closing costs or total loan amount. It is the same concept with PACE financing. The difference is that PACE may have a long gap of time in which interest accrues due to the annual property tax schedules.

There are two potential scenarios related to the tax roll cut-off dates in your county and your PACE application.

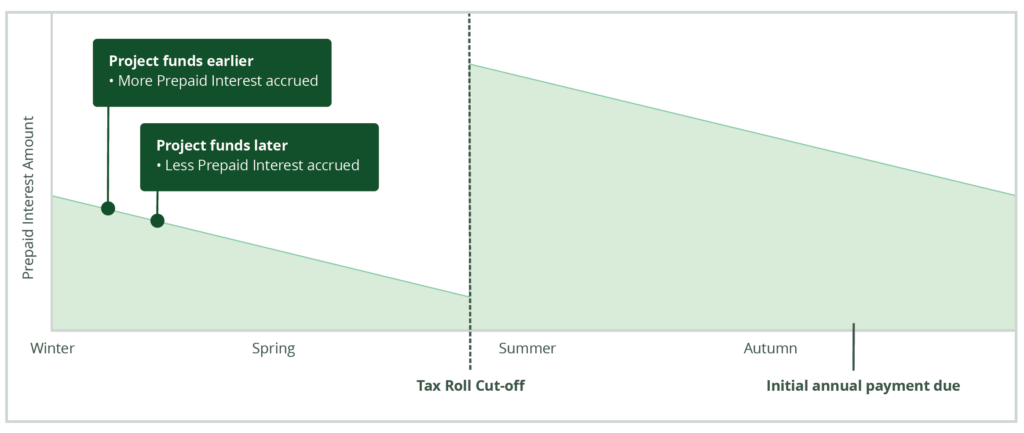

1) The estimated window for when your project will fund does not span the tax roll cut-off date in your county. This is usually if your project funds in the autumn or winter.

2) The second is when the estimated window for when your project will fund does span the tax roll cut-off in your county. This is usually if your project funds in the spring and early summer.

A project funds once:

• The contractor finishes the project and submits all final documentation to Renew Financial;

• You approve of the project by signing the Completion Certificate;

• Renew Financial approves the final documentation, and Renew Financial pays your contractor for the project.

555 12th St, Suite 1650, Oakland, CA 94607

Monday–Friday: 5am to 7pm PT

Saturday-Sunday: 7am to 3:30pm PT