Homeowners looking to finance their home improvement and energy efficiency upgrades have multiple lending options available and should carefully consider interest rates, repayment terms, fees, and consumer protections, among other factors. Understandably, most homeowners want this step of their home improvement project to be simple and easy and the right choice for them. So, how do other financing choices actually stack up to the flexibility and benefits of Property Assessed Clean Energy (PACE) financing?

Let’s take a look at how PACE financing compares to solar loans, general and subprime unsecured loans, credit cards, and home equity lines of credit (HELOC).

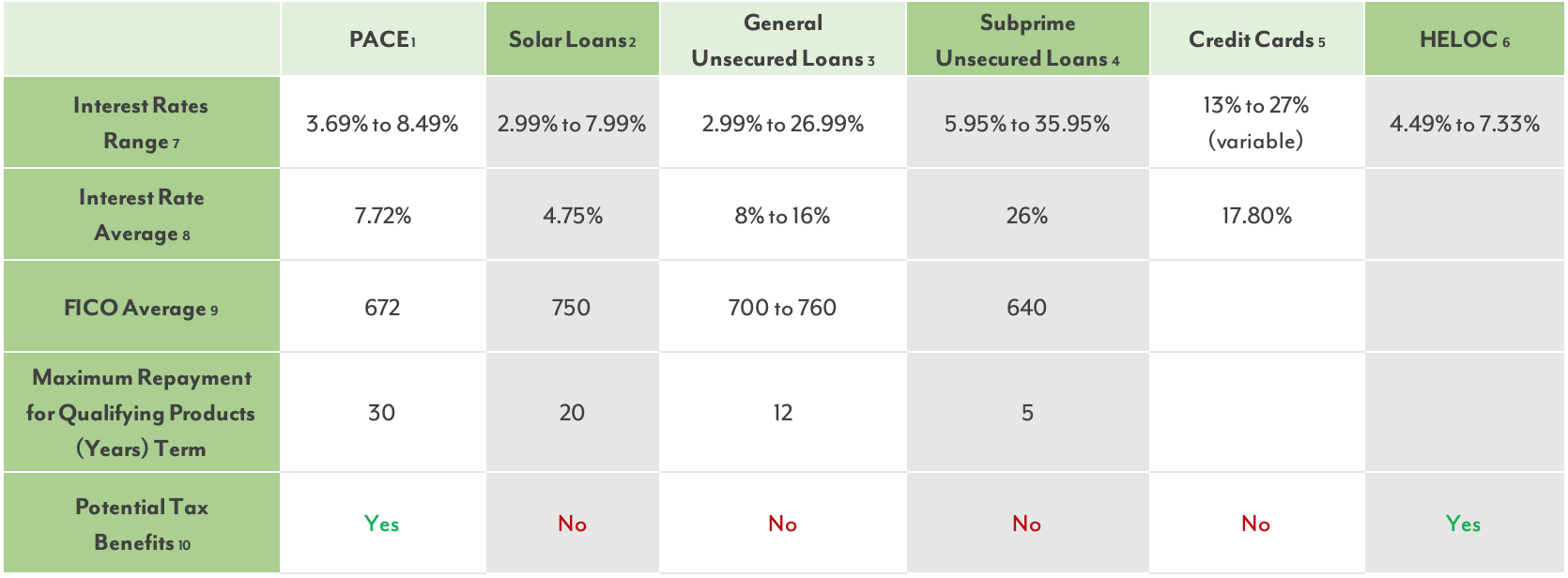

Compare PACE Financing:

Credit Score

Unlike many other traditional financing options, interest rates for PACE financing are not determined primarily by the borrower’s credit history. Instead, it is a combination of things, and the available equity in your home plays a larger role in determining your PACE interest rate.

Since having a less than stellar FICO score is not a problem or barrier to access, PACE financing is often an attractive option for many homeowners who have built-up equity in their homes. In other words, PACE is a great option for those who want access to an affordable fixed-interest rate but find that alternative options, like credit cards and unsecured loans, don’t take into account the wealth in their homes and only offer much higher interest rates.

Interest Rates & Repayment Terms

When comparing interest rates across traditional lending choices, PACE financing offers among the lowest range – on average from 3.69% to 8%. While some solar loans can be competitive, PACE is a real steal when the top range of projects financed through unsecured loans and credit card loans can be often two to three times higher and even can reach up to 20%, depending on your credit history.

PACE also gives homeowners flexible fixed repayment terms usually between 5 and 30 years – whatever works best for them and is consistent with the expected useful life of the project. Plus, there are no early repayment penalties or balloon payments for projects financed through PACE. This means you can freely choose a repayment term length that works best for you based on the payment amount, without any surprises down the line.

Upfront Costs

Another way to reduce the interest rate on traditional financing options is with a down payment. However, for homeowners who may not be in a position to make a large down payment, or simply prefer not to, PACE is often a better choice. As mentioned, there are no required upfront costs for PACE financing and homeowners can always finance up to 100% of the costs of their projects. With PACE you can, therefore, reap all the immediate benefits and repay the costs gradually over time.

Customer Support & Protections

PACE also offers strong consumer protections for homeowners. Indeed, a critical differentiator between PACE financing and HELOCs, credit cards, and solar loans is the standards of customer protection support that comes with PACE financing. Renew Financial offers clear financial disclosures, safeguards against unsatisfactory contractor work, and direct customer support to ensure that you, the homeowner, are protected every step of the way.

This goes above and beyond other financing options, providing you the critical resources you need to stay in the driver’s seat. Does Your Next Project Qualify for PACE?

The flexibility of PACE applies to a wide range of home improvements from solar, HVAC, storm windows, and roofs that will increase the safety, efficiency, and comfort of your home while giving you the ability to repay your project costs conveniently overtime at an affordable fixed-interest rate. Choose a project, and ask the experts at Renew Financial how you can get started today.

Looking for the home improvement financing option that will work for you? Ask Renew Financial about PACE, today. Call 844-736-3934.

1. Renew Financial actuals as of 5/6/19.

2. Solar Mosaic, Dividend Finance and LoanPal are examples of this type of solar loan.

3. GreenSky, Prosper and Service Finance are examples of this type of unsecured loan.

4. Avant and Lending Club are examples of this type of loan.

5. Summary of credit cards for Fair, Good and Excellent credit scores at https://www.bankrate.com/credit-cards/todays-best-credit-cards/ and https://www.bankrate.com/credit-cards/current-interest-rates/ as of 5/6/19.

6. Summary of Home Equity Loans available at https://www.bankrate.com/home-equity.aspx as of 5/6/19.

7. Interest rate ranges reflect 10 to 20-year repayment terms, including all available sellers point options.

8. Unless noted elsewhere, data is based on a sample of recent product data from actual providers listed above and other peers. Subprime data is for actual products with 640 average FICO®.

9. Renew Financial actual data, including all PACE financings provided in all markets since the launch. All others are approximated based on a sample of recent product offerings.

10. Potential tax benefits include the home mortgage interest expense deduction. Not all applicants will be eligible. Consult your tax advisor.

Important Disclosures

PACE financing is subject to credit approval. Underwriting requirements and restrictions apply. PACE financing is secured by a lien on the subject property and may be required to be repaid upon refinance or sale. Homeowners should perform due diligence before selecting a home improvement contractor. PACE financing is private financing that must be repaid in full. PACE financing is not a government subsidy. Homeowners are encouraged to use PACE financing responsibly. Names or trademarks used above are the property of their responsive owners.