There are already many details to juggle when it comes to planning your next home improvement project, so adding the task of sifting through financing details can be intimidating. Renew Financial offers homeowners many resources when it comes to choosing the right financing options for their home’s efficiency, safety, and health upgrades. Below, we take a look at how PACE financing compares to a Home Equity Loan and what factors should be considered.

A common misconception about home equity loan options is that a strong credit score is the primary determining factor when it comes to securing low-interest rates, favorable repayment terms, and low upfront costs. However, the credit score is only part of the equation and depending on the home equity loan provider, there are many other factors that will contribute to the overall convenience and affordability of a loan.

Common Loan Factors

A financing provider may weigh the following factors in determining the interest rate, APR, and terms of a home equity loan:

Loan-to-value (“LTV”) ratio: LTV is the amount of equity tied up by the primary mortgage or other primary property-secured debt. Determining the LTV is simple: Take the outstanding balance on the primary mortgage or property-secured debt and divide it by the home’s market value.

For example, if there is an outstanding balance of $250,000 on a home that is currently appraised at a value of $400,000, the LTV is 250,000➗400,000 = 62.5%.

In essence, the less owed on a mortgage in relation to the current value of the home, the better. An LTV of 80% or less can in some cases offer favorable financing terms.

Combined Loan-to-Value (“CLTV”) ratio: CLTV is the amount of equity tied up by a mortgage, plus all other existing and potential new property-secured debt (such as a home equity loan). This is a projection of what your new LTV ratio would be if approved for the loan.

Financing companies use the CLTV to determine a borrower’s risk of defaulting on a loan when more than one loan is in place. A CLTV of 80 percent and above will oftentimes see higher interest rates, and some traditional financing companies are more likely to approve a borrower with a high credit score and low debt-to-income ratio (see below).

Debt-to-Income (“DTI”) ratio: DTI is the borrower’s amount of debt compared to their gross monthly income (income before taxes and other deductions), excluding living expenses or other everyday budgetary considerations, like utility costs.

Traditional financing companies use a DTI ratio to calculate the borrower’s ability to repay the financed amount. Borrowers with a 36% or lower DTI usually have the advantage to receive the most favorable financing terms.

Comparing PACE to Traditional Home Equity Loans

Now that you have a better understanding of how each of these variables can affect the financing terms you may get for a home equity loan, let’s look at a hypothetical borrower’s scenario.

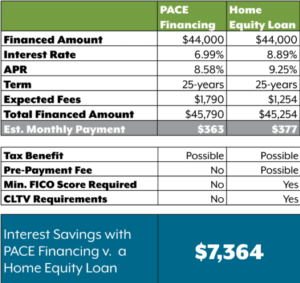

We’ve taken some example PACE interest rates, fees, and monthly payments based on rates offered by registered master contractors for a 25-year repayment term (actual rates can vary between 6.69% and 8.49% depending on project size and repayment terms), and home equity loan rates based on SpringEQ loans as advertised in December of 2019, and stacked them up using the following fictional homeowner financial attributes:

FICO score: 740-749

Loan-to-value (LTV) ratio: 80%

Finance amount needed for a new roof: $44,000

While the homeowner did have a seemingly favorable LTV ratio of 80%, when accounting for the CLTV of the forthcoming home equity loan, it was over the 90% mark. This high CLTV ratio can push the home equity loan interest rate to 8.89% or above, resulting in $7,364 added to the cost of the loan over the 25-year period compared to PACE. Notice, there is an initial savings of $536 in expected fees, but these savings are far eclipsed by the interest rate over the term length.

Interest rates for PACE financing are not dependent on the CLTV, which means that homeowners can rest easy knowing that their interest rate will not fluctuate based on their CLTV alone.

Do You Need a Good Credit Score to Qualify for PACE?

In the end, credit scores are not the only determining factor when it comes to PACE financing or home equity loans.

While PACE financing may not always be the best option for every situation, it can offer advantages over some home equity loans, or other traditional financing options like personal lines of credit. Plus, PACE financing comes with built-in safeguards to protect homeowners from unsatisfactory contractor work, or misunderstandings and misconceptions when it comes to the details of your home improvement financing.

Think PACE financing may be right for your next project? Call Renew Financial today at (844) 736-3934.

– – – – – –

Important Disclosures:

Interest Rate: Interest rates as of December 6, 2019. The interest rate used for PACE financing is based on the base rate offered by a Master registered contractor for a 25-year repayment term. Available interest rates depend on your project size and repayment term. Available interest rates range between 6.69% and 8.49%. The interest rate used for the Home Equity Loan was advertised by SpringEQ loans on www.bankrate.com and it was based on the credit score and LTV characteristics of our shopper mentioned above. The use of the SpringEQ trade name or trademark is for identification and reference purposes only and does not imply any association with the trademark holder of their product brand.

Expected Fees: The fees displayed do not include prepaid interest between the time of closing and the first payment due. The fees in the total include but are not limited to: origination fees, recording fees, etc. The fees for the Home Equity Loan are based on the fees SpringEQ quoted to our shopper.

Monthly Payment: The monthly payment represented for PACE financing is only for illustrative purposes, the annual payment of $4,358.96 was divided by 12 monthly payments. The payment for PACE is due under the same schedule as the property taxes are (annual or biannual).

Interest Savings: The total interest paid over the life of the PACE financing is $60,375.82. The total interest paid over the life of the Home Equity Loan is $67,739.48. These calculations include the amount of prepaid interest between the time of closing and the first payment due.

The comparison provided only to illustrate the impact of CLTV. Interest savings not guaranteed. Actual results may vary. PACE financing is subject to credit approval. Underwriting requirements and restrictions apply. PACE financing is secured by a property lien until repaid in full. PACE financing may be required to be repaid upon refinance or sale. Homeowners should perform due diligence before selecting a home improvement contractor. PACE financing is private financing that must be repaid in full. PACE financing is not a government subsidy.